UPA's Policy Paralysis

The Indian economy is slowing down. GDP in the second quarter grew by 6.9% over the corresponding period last financial year. Economic growth is being impacted by a variety of reasons, including the eurozone Debt Crisis. However, there is another major macroeconomic parameter that is giving sleepless nights to the government: high rate of inflation.

Inflation relates to the sustained rise, over a period of time, in the general price level when there is a rise in demand (for goods) without an equal rise in supply.

In today’s interconnected world, a general lack of stability in the prices of goods and services characterises all types of economies, be it an emerging economy like India or an advanced economy like the United States or for that matter, an underdeveloped economy like that of Senegal. But as we all know, any kind of uncertainty, including price instability, is not good for business and economy.

Generally, there is never a single cause behind the sustained rise in prices of a basket of goods and services, like wheat, rice, and cooking oil. However, some general reasons include:

(a) increase in money supply;

(b) rise in government spending;

(c) rise in purchasing power (a direct result of rising incomes);

(d) low supply across a range of goods, and

(e) infrastructure issues.

To add to these, black-marketing, hoarding, speculation, and exploding population have all contributed to a rise in demand for goods and services. In India, inflation is seen as a result of a combination of all these factors.

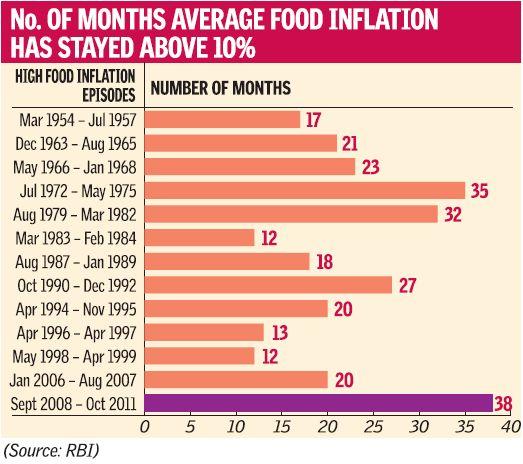

India has been experiencing very high rates of food inflation. Food inflation impacts just about everybody, of course except the rich and the privileged. The graph below shows the number of months where the average food inflation has stayed above 10%.

It is easy to gather that the country experienced double digit inflation in the first two decades after independence. In the years before the Green Revolution brought in some degree of self-reliance in foodgrain production, India was an inward-looking, resource scarce economy, characterised by improper logistics and transportation channels.

However, what is disconcerting is that today India is in the midst of the longest run of double-digit inflation, since independence. This has impacted millions of people, especially the poor and vulnerable. Rapidly rising inflation leads to a fall in the purchasing power of money. With an unemployment rate of 10.8%, it surely is adding misery and bringing down the overall quality of life, as people shun expensive but necessary grains and cereals and substitute with alternatives that are cheap but do not lend adequate nutrition.

The government has utterly failed to rein in the galloping inflation. There is not a day when the PM and his ministers do not promise to bring down the inflation rate and lower the sweep of its attendant misery on millions of hapless citizens.

The imbroglio over the hastily-made decision on FDI in multibrand retail, depreciating rupee, plunging industrial production, creaking infrastructure, and rampant corruption all reflect the enormous policy paralysis at the Centre.

The Prime Minister, Dr Manmohan Singh, and the Super Prime Minister, Sonia Maino Gandhi, puppet and puppet-master respectively, are busy saving P. Chidambaram, Kapil Sibal, and other CONgressmen from the various corruption scandals that have hit the UPA with full force.

When the puppet PM and his Puppet-Master are busy saving their own skin and kin, will they worry about the struggling common people of this nation? You know the answer; don't you?

(Read The Explainer: Inflation)

Source for infographic: Business Line